{kind=link}

Current bank accounts are trendy among companies, firms, public enterprises, and business people who generally have higher numbers of regular transactions with the bank. Because of these accounts’ fluidity, they don’t earn any interest. These also usually do not limit the number of trades made. The current version being a zero account is generally associated with huge transactions regularly.

Table of Contents

What Is a Current Bank Account?

A current account is a deposit account offered by banks worldwide, primarily designed for:

- Businesses

- Entrepreneurs

- Professionals with frequent transactions

Unlike savings accounts, it is built for cash flow management—not wealth growth.

| Element | Explanation |

| Account Type | Deposit account |

| Primary Purpose | Daily transactions |

| Interest | Usually none |

| Users | Businesses, professionals |

| Liquidity | Very high |

| Transaction Limits | Unlimited |

Globally, current accounts are also called:

- Checking accounts (USA, Canada)

- Transaction accounts (Australia)

How a Current Bank Account Works

A current account functions as a financial operating system for daily money movement. A current account prioritizes speed and flexibility over returns.

Key Features of a Current Bank Account

| Feature | Description | Why It Matters |

| Unlimited Transactions | No cap on deposits/withdrawals | Ideal for businesses |

| No Interest | Funds don’t grow | Trade-off for liquidity |

| Overdraft Facility | Borrow short-term funds | Cash flow support |

| High Minimum Balance | Higher than savings | Bank risk management |

| Multi-User Access | Authorized signatories | Team operations |

| Digital Banking | Online, mobile, API access | Efficiency |

According to banking sources, current accounts are designed to handle “high transaction volumes with immediate access to funds” rather than savings accumulation.

What are the Charges to Open a Current Account?

| Charge Type | Typical Cost (Global Range) | When It Applies | Notes |

| Account Opening Fee | Free – $100 (₹0 – ₹8,000) | At account setup | Many banks offer free opening, especially online or for startups |

| Minimum Balance Requirement | $100 – $10,000+ (₹5,000 – ₹8L+) | Ongoing | Varies widely by account type (basic vs premium) |

| Monthly Maintenance Fee | $0 – $30/month (₹0 – ₹2,500) | Monthly if balance not maintained | Can be waived if minimum balance is maintained |

| Non-Maintenance Penalty | $5 – $50/month (₹200 – ₹4,000) | If balance falls below requirement | Example: ~₹1,500/quarter in some banks (HDFC Bank) |

| Cash Deposit Charges | Free up to limit, then 0.2%–2% | After free monthly limit | Example: ₹3.5 per ₹1,000 beyond limit |

| Cash Withdrawal Charges | Free or $1–$5 per transaction | Non-home branch / excess usage | Often free within limits |

| Transaction Fees (Transfers) | Free – $5 per transfer | Depends on method (online vs branch) | Online transfers often free |

| Cheque Handling Charges | $0 – $10 per cheque | Bounce, stop payment, clearing | Bounce penalties are higher |

| Overdraft Charges | $10 – $35 per use | When overdraft is used | Common in US/UK accounts |

| Account Closure Fee | $0 – $50 | If closed early (within 6–12 months) | Many banks waive after 1 year |

| Foreign Transaction Fee | 0.5% – 3% | International payments | Higher for currency conversion |

| Miscellaneous Charges | $1 – $20 per service | Statements, certificates, etc. | Depends on usage |

Current Account vs Savings Account

This is where most users get confused. Using a current account for savings is a financial inefficiency.

| Feature | Current Account | Savings Account |

| Purpose | Transactions | Saving money |

| Interest | None or minimal | Moderate |

| Transactions | Unlimited | Limited |

| Minimum Balance | High | Low |

| Overdraft | Available | Rare |

| Users | Businesses | Individuals |

| Risk Level | Low liquidity risk | Moderate |

Types of Current Accounts

Different countries and banks offer variations. Globally, these variations exist to match different business scales and transaction volumes.

| Type | Best For | Key Feature |

| Standard Current Account | Small businesses | Basic features |

| Premium Current Account | Large enterprises | High limits + perks |

| Zero Balance Account | Startups | No minimum balance |

| Merchant Account | Retail businesses | Payment gateway integration |

| Foreign Currency Account | Import/export firms | Multi-currency support |

| Packaged Account | SMEs | Bundled services |

Benefits of a Current Account

| Benefit | Explanation | Business Impact |

| High Liquidity | Instant access to funds | Faster operations |

| Cash Flow Management | Track inflow/outflow | Better decisions |

| Overdraft Support | Short-term credit | Prevent disruptions |

| Professional Credibility | Business identity | Builds trust |

| Bulk Transactions | Payroll, vendor payments | Efficiency |

| Integration | Accounting tools, APIs | Automation |

A current account is considered essential infrastructure for business operations, enabling seamless financial transactions.

Drawbacks

| Drawback | Explanation | Impact |

| No Interest | Funds don’t grow | Opportunity cost |

| High Balance Requirement | Maintenance needed | Penalties if unmet |

| Service Charges | Transaction fees | Increased costs |

| Not Ideal for Individuals | Overkill for low usage | Inefficient |

A current account is powerful—but only when used correctly.

Who Should Use a Current Bank Account?

Ideal Users Table

| User Type | Why It Fits |

| Business Owners | Frequent transactions |

| Freelancers | Multiple client payments |

| Startups | Cash flow management |

| Traders | High-volume activity |

| NGOs / Organizations | Fund management |

Not Ideal Users Table

| User Type | Reason |

| Students | Low transaction needs |

| Salaried Individuals | Better with savings account |

| Passive Investors | Need interest-based accounts |

Current Account vs Checking Account

Many beginners confuse terminology. Functionally, they are nearly identical, with minor regulatory differences.

| Region | Term Used |

| USA | Checking Account |

| UK / India | Current Account |

| Australia | Transaction Account |

Common Misconceptions

| Myth | Reality |

| Only companies can open it | Individuals can too |

| It’s better than savings | Depends on usage |

| No benefits | Offers liquidity + flexibility |

| It’s mandatory for business | Not always, but recommended |

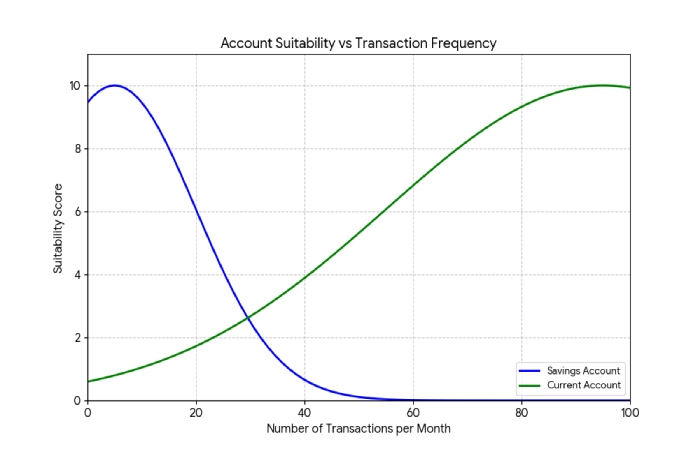

When Should You Switch to a Current Account?

| Situation | Switch? |

| 5–10 transactions/month | No |

| 20–50 transactions/month | Maybe |

| 50+ transactions/month | Yes |

| Running a business | Strongly yes |

| Need overdraft | Yes |

Advanced Insight

Here’s what most articles miss:

A current account is not a financial product—it’s a layer of financial infrastructure.

At scale:

- Businesses don’t optimize for interest

- They optimize for speed, liquidity, and reliability

That’s why:

- Corporations keep millions in current accounts

- Despite earning zero interest

Because cash flow > returns in operations.

FAQ

What does “current” mean in banking?

It refers to ongoing, frequent financial transactions, not time.

Is a current account the same as a checking account?

Yes, functionally similar—different terminology by region.

Do current accounts earn interest?

Generally, no, as they prioritize liquidity.

Can individuals open a current account?

Yes, especially freelancers and professionals.

Why do businesses prefer current accounts?

They allow unlimited transactions and better cash flow management.

Final Verdict

A current account is essential for managing money in motion, not money at rest. If your financial life involves frequent transactions, business operations, or cash flow complexity, it becomes a non-negotiable tool. But if your goal is saving or growing wealth, a current account is the wrong choice.