{kind=link}

The term “Upgrade Credit Card” is misleading—and that’s exactly why it ranks so high in search. Most users expect a traditional credit card, but what they actually get is something fundamentally different.

The Upgrade Card, issued by Upgrade Inc., is a hybrid financial product that blends a credit card interface with a personal loan repayment structure. According to NerdWallet, it’s best understood as a system of “closed-end loans accessed through a card”, rather than a revolving credit account.

This distinction is not just technical—it completely changes how interest works, how you repay debt, and how you should evaluate the product strategically.

Table of Contents

What Is the Upgrade Credit Card?

At a surface level, the Upgrade Card looks like any Visa credit card:

- You can swipe it in stores

- Use it online

- Access a credit limit

But behind the scenes, each purchase becomes a fixed-term installment loan instead of revolving debt.

| Action | What Happens |

| You spend ₹10,000 equivalent | Converted into a fixed loan |

| Interest applied | Fixed APR (not revolving) |

| Repayment | Equal monthly installments |

| Credit reuse | Available again after repayment |

This structure removes the traditional “minimum payment trap” found on typical credit cards.

How the Upgrade Card Works

Understanding the workflow is key to understanding whether this card is right for you.

| Step | Process | Strategic Impact |

| 1 | Purchase made | Works like a normal card |

| 2 | Converted to loan | No revolving balance |

| 3 | Fixed repayment term | Predictable payoff |

| 4 | Monthly EMI paid | Reduces principal steadily |

| 5 | Credit becomes reusable | Similar to a credit line |

Unlike traditional cards, you cannot carry a balance indefinitely—each transaction is locked into a repayment schedule.

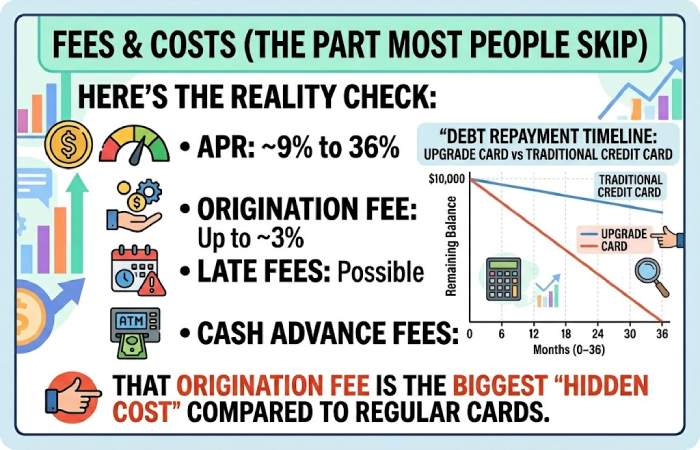

Fees and Costs (The Part Most People Skip)

Here’s the reality check:

That origination fee is the biggest “hidden cost” compared to regular cards.

Key Features of Upgrade Card

1. Fixed APR

Most Upgrade cards offer APR ranges around: 14.99% – 29.99% depending on creditworthiness

| Feature | Traditional Card | Upgrade Card |

| Interest type | Variable, compounding | Fixed |

| Monthly variability | High | Low |

| Transparency | Low | High |

You always know your exact repayment timeline and cost upfront.

2. Installment-Based Repayment

Instead of paying: Minimum due (e.g., 5%)

You pay: Fixed monthly EMI (like a personal loan)

Comparison

| Payment Type | Outcome |

| Minimum payment (credit card) | Long-term debt |

| Fixed EMI (Upgrade) | Forced payoff |

This is a behavioral design feature, not just a financial one.

3. Credit Line Structure

Upgrade provides a reusable credit line:

- Typical range: $500 – $25,000

- Most users fall below ~$15,000

Important Difference

| Feature | Traditional Card | Upgrade Card |

| Credit utilization | Reported | Not always reported same way |

| Credit type | Revolving | Installment |

| Replenishment | Automatic | Conditional |

This can impact your credit score differently.

4. Charges

Many blogs underplay this section—don’t.

| Fee Type | Typical Range |

| APR | 14.99% – 29.99% |

| Balance transfer fee | Up to 5% |

| Foreign transaction | Up to 3% |

| Late fee | Up to $29 |

Even though there’s often no annual fee, transaction-related fees can still add up.

5. Rewards

Compared to premium cards, rewards are not competitive. Upgrade offers limited rewards depending on the variant:

| Card Type | Reward Structure |

| Cash Rewards | ~1–1.5% cashback |

| Triple Cash | Up to 3% categories |

| Life Rewards | Category-based cashback |

The Core Truth: It’s a Loan Disguised as a Credit Card

According to NerdWallet, The Upgrade Card is essentially a series of closed-end loans accessed via a credit line. This is why it appeals strongly to debt-conscious users.

| Aspect | Reality |

| Marketing | Credit card |

| Structure | Personal loan system |

| User behavior | Controlled spending |

| Risk model | Reduced revolving debt |

Who Should Use the Upgrade Credit Card?

1. Beginners with Poor Credit Discipline

| Problem | Upgrade Solution |

| Overspending | Fixed repayment |

| Minimum payment trap | Eliminated |

| Debt anxiety | Predictable payoff |

2. Debt Consolidation Users

| Need | Benefit |

| Structured payoff | Fixed timeline |

| Simplicity | One payment |

| Lower chaos | No revolving balance |

3. Credit Builders

Upgrade reports payments to credit bureaus:

- Helps build payment history

| Credit Factor | Impact |

| Payment history | Positive |

| Utilization | Less impact |

| Mix of credit | Improved |

Not Ideal For

1. Rewards Maximizers

| Reason | Explanation |

| Low cashback | Compared to premium cards |

| No bonuses | Limited incentives |

2. Financially Disciplined Users

If you:

- Pay full balance monthly

This card gives you zero advantage

3. Short-Term Borrowers

| Issue | Why |

| Fixed term | Less flexibility |

| Early payoff | Not always optimized |

Upgrade Card vs Traditional Credit Cards

| Feature | Upgrade Card | Traditional Credit Card |

| Core Structure | Hybrid (credit card + personal loan) | Revolving credit |

| How Debt Works | Each purchase becomes a fixed installment loan | Balance revolves month-to-month |

| Interest Type | Fixed APR per transaction | Variable APR (can change over time) |

| Repayment Style | Fixed monthly payments (EMI-like) | Minimum payment + optional full payment |

| Debt Duration | Fixed (e.g., 12–36 months) | Open-ended (no fixed payoff timeline) |

| Minimum Payment Trap | Not possible | Common issue |

| Interest Predictability | High (known upfront) | Low (depends on usage & rates) |

| Flexibility | Lower (structured repayment) | High (pay any amount above minimum) |

| Credit Limit Usage | Reusable after repayment | Continuously revolving |

| Rewards System | Limited (1–3% cashback) | Strong (points, travel, cashback, bonuses) |

| Fees | May include transfer/late fees | Wide range (annual, late, foreign, etc.) |

| Best For | Debt control & beginners | Rewards, flexibility, advanced users |

| Worst For | Rewards optimization | People with poor payment discipline |

| Psychological Effect | Forces disciplined repayment | Encourages flexible (sometimes risky) spending |

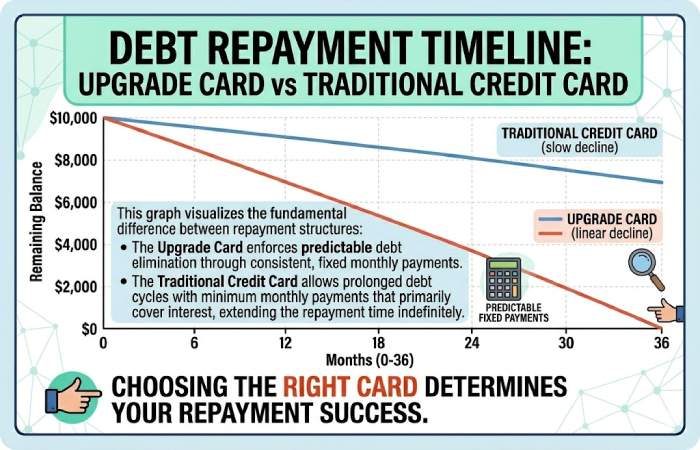

Debt Repayment Timeline: Upgrade Card vs Traditional Credit Card

Real-World Use Case

Scenario: ₹1,00,000 Purchase

| Factor | Traditional Card | Upgrade Card |

| Payment style | Minimum due | Fixed EMI |

| Debt duration | Uncertain | Fixed (e.g., 24 months) |

| Interest | Compounding | Fixed |

| User stress | High | Lower |

Upgrade reduces uncertainty, not necessarily cost.

Pros and Cons

Pros

| Benefit | Why It Matters |

| Predictable payments | Easier budgeting |

| Debt control | No revolving trap |

| Credit building | Reports to bureaus |

| Beginner-friendly | Structured system |

Cons

| Drawback | Impact |

| Less flexibility | Locked repayment |

| Fees | Transfer + late fees |

| Lower rewards | Not ideal for optimization |

| Not true credit card | Misleading expectations |

Is the Upgrade Card Safe and Legit?

Yes, it is legitimate.

- Issued through partner banks

- Accepted where Visa is accepted

- Includes fraud protection policies

According to NerdWallet:

- It is a valid and regulated financial product

Final Verdict

The Upgrade Credit Card from Upgrade Inc. isn’t a traditional credit card—it’s a structured borrowing tool designed to turn everyday spending into fixed, predictable repayments. That makes it highly effective for beginners or anyone struggling with revolving debt, as it removes the minimum payment trap and enforces disciplined payoff.

However, this same structure limits flexibility and offers weaker rewards compared to standard credit cards, meaning financially disciplined users who pay balances in full each month will gain little value. In essence, it’s best viewed not as a better credit card, but as a smarter alternative for users who prioritize control over optimization.